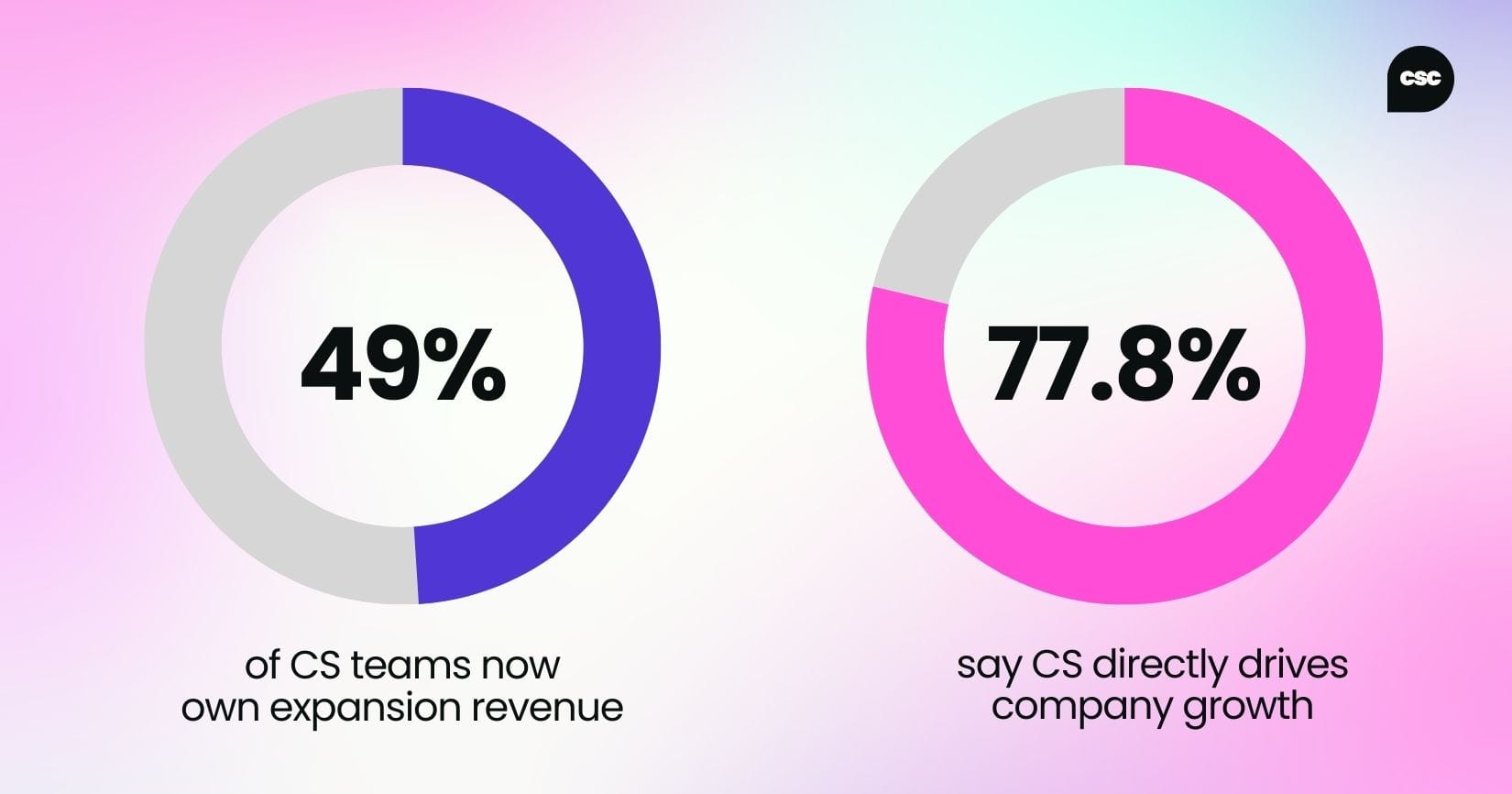

Customer success (CS) has never been more commercially accountable. Nearly half of CS teams now own expansion revenue. Almost 80% believe they directly drive company growth.

Leadership representation continues to increase. And yet, across many organizations, the cultural center of gravity is shifting in the opposite direction – back toward sales-led growth. In 2025, we saw customer-first cultures decline. It’s a bit of a head-scratcher, right?

For many CS leaders, this shift feels familiar: expansion targets are rising, but influence over deals, segmentation, and product priorities often isn’t rising with them.

Data shows a 13% increase in sales-led environments and a double-digit drop in customer-first orgs. That juxtaposition matters because it suggests that while CS is being positioned as a revenue engine, the broader cultural environment is shifting in ways that may complicate that mandate.

What’s driving the rise of sales-first culture?

As budgets tightened and growth became harder to secure, many organizations responded by doubling down on acquisition. In uncertain markets, new revenue often feels more controllable than long-term value realization. Pipeline can be tracked daily. Bookings are visible. Forecasts are immediate.

By contrast, customer value accrues over time. Adoption, expansion, and retention depend on alignment across multiple teams. Disappointingly, the results are less instantaneous.

Under pressure, organizations tend to prioritize the lever that appears most directly tied to short-term outcomes. In 2025, that lever was sales.

And the wider revenue ecosystem shows similar signals. According to the 2025 Revenue Operations Landscape Report, more than half (57.8%) of revenue leaders say ARR or MRR is the most effective metric for engaging executive leadership.

While these metrics capture recurring revenue overall, they rarely distinguish whether growth is driven by acquisition or customer retention. As a result, leadership conversations often focus on ARR growth while the underlying drivers of that growth receive less scrutiny.

This doesn’t necessarily reflect a philosophical rejection of customer-centricity. Rather, it reflects a recalibration under economic strain. However, when that recalibration persists, it begins to reshape how teams are resourced, how influence is distributed and how growth is defined.

Customer-first culture vs sales-first culture: What’s the difference?

Framing this as a binary choice between caring about customers and caring about revenue would be misleading. Both cultures are commercially oriented. The difference lies in where growth responsibility is anchored and how investment follows that responsibility.

In a customer-first culture, growth is driven through long-term value delivery. Retention is treated as a primary growth engine. Expansion follows adoption and realized outcomes. Product feedback loops are structured and prioritized. Customer success has visibility at the executive level and influence over strategic decisions.

In a sales-first culture, growth is organized around acquisition velocity. Revenue targets are front-loaded. Sales performance heavily influences internal priorities. Post-sale teams like success, support and experience, often inherit the outcomes of deals structured under time pressure. Investment decisions tend to favor pipeline acceleration over post-sale infrastructure.

Neither model is inherently flawed. The challenge emerges when acquisition intensity increases without proportional investment in post-sale systems.

And that is where the 2025 data becomes particularly revealing.

The structural tension beneath the cultural shift

At the same time that sales-first cultures rose:

- 49% of CS teams reported owning all expansion revenue

- 78.7% believe CS is a key revenue driver

But the infrastructure isn't keeping pace:

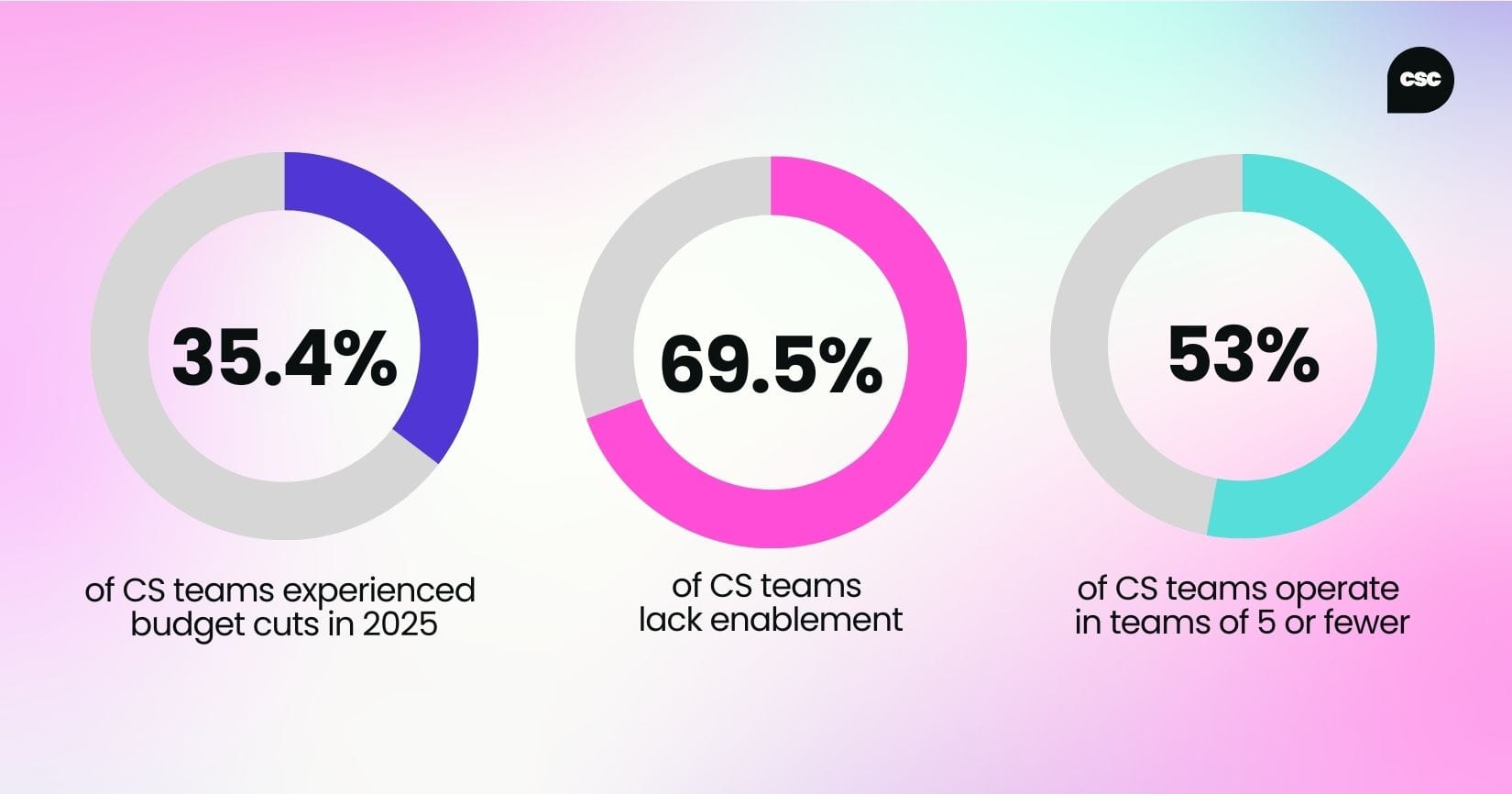

- 35.4% experienced budget cuts

- 69.5% lack a formal enablement function

- 53% operate in teams of five or fewer

This combination is difficult to ignore. Customer success is being positioned as a commercial engine, increasingly responsible for renewals, upsells and cross-sales. Yet many of these teams are operating with constrained resources, limited enablement support, and growing account portfolios.

In effect, revenue accountability is rising in environments that are simultaneously becoming more sales-oriented.

This creates an unpleasant structural tension. For one, account expansion ownership implies influence and investment. But in practice, enablement, operations, and headcount have not scaled proportionally with expectations.

When revenue responsibility grows faster than infrastructure, ambiguity follows. Who owns the long-term growth strategy? Who defines the ideal customer profile? Who actually sets expansion targets? Who qualifies for an upsell? Without clarity, culture drifts toward whichever function holds the most immediate leverage.

The incentive design problem

One reason this dynamic persists is simpler than culture alone: incentives.

Organizations often describe themselves as “customer-first,” but compensation structures tell a different story.

If sales teams are comped almost entirely on new ARR and AEs carry little or no accountability for retention or expansion outcomes, sales-first behavior is not a cultural failure. It’s rational behavior.

If CS owns expansion revenue on paper but receives weaker variable compensation, less tooling investment, and fuzzier targets, then “revenue accountability” becomes symbolic rather than structural.

And if executive bonuses are tied primarily to in-year bookings rather than multi-year NRR or lifetime value, organizations will predictably re-center on acquisition whenever pressure intensifies.

Organizations rarely become sales-first by accident. They become sales-first because incentives make it rational.

The long-term risk of short-term emphasis

Sales-first acceleration can generate visible momentum. New logos energize organizations. Bookings validate strategy. Revenue spikes reinforce executive confidence.However, the downstream effects are less visible in the short term.

If acquisition targets outpace qualification rigor, ICP drift can occur. If onboarding capacity lags behind closed deals, early adoption slows. If product feedback loops are deprioritized, misalignment compounds quietly. Over time, these factors surface in tangible churn metrics and net revenue retention.

But there’s also a quieter operational cost that rarely appears in dashboards: the invisible tax of an unchecked sales-first culture.

This tax often shows up in three places:

- Burnout among CS teams asked to own commercial outcomes without authority over deal qualification or product priorities.

- Constant firefighting as post-sale teams unwind oversold deals or rescue struggling implementations.

- Erosion of customer trust during the handoff from optimistic sales messaging to operational reality.

These costs may not appear immediately in revenue reports, but they accumulate through slower implementations, unpredictable accounts, and employee turnover.

The State of Customer Success 2025 data already points to familiar internal barriers:

- Lack of clarity around CS roles and priorities

- Poor leadership understanding of the CS function

- Product misalignment

- Siloed communication between departments

- Under-resourcing

These challenges aren’t by any means new, but they certainly intensify when acquisition pressure dominates organizational focus.

Granted, a sales-first culture doesn’t automatically lead to higher churn. Yet without deliberate alignment between acquisition and retention, the risk profile increases exponentially.

Is customer-first culture disappearing, or evolving?

Although customer-first cultures declined by more than 11 percentage points year-over-year, nearly one-third of organizations still identify as customer-first.

This suggests that customer-centricity isn't vanishing. Rather, it may be undergoing reinterpretation.

As customer success becomes more commercially integrated, some organizations may no longer separate “customer-first” from “revenue-first.” Retention is revenue. Expansion is revenue. Adoption is revenue.

In high-performing environments, these concepts reinforce one another. Customer-first thinking drives measurable revenue outcomes. Revenue accountability strengthens the strategic position of CS.

The real issue isn’t whether companies prioritize sales or customers. It’s whether acquisition and retention operate as a unified system, or as competing priorities with separate clocks.

Sales performance is measured quarterly. Customer value unfolds over the years. When short-term incentives dominate long-term capacity, an imbalance appears.

Growth system design as a leadership discipline

At the executive level, this tension increasingly becomes a question of system design.

Who’s actually responsible for designing the full growth system from ICP definition to deal qualification, then on to onboarding and value realization, culminating with expansion?

In many organizations, these stages remain fragmented across departments. Sales optimizes for bookings. Customer success optimizes for adoption. Product optimizes for roadmap velocity. Marketing optimizes for lead generation.

Each team performs amiably within the confines of its own metrics, but the overall system may remain misaligned. This is where high-performing organizations truly shine; they approach it differently. They treat growth as an end-to-end system with shared accountability for net revenue retention.

Systemic decisions often look counterintuitive in the short term. Tightening ICP criteria, slowing low-fit acquisition, or investing more heavily in onboarding may reduce new ARR in a single quarter. But over the following four to six quarters, these decisions frequently produce stronger NRR, healthier expansion, and higher sales efficiency.

Voice of the customer in a sales-first environment

Another telling data point concerns voice-of-customer (VoC) programs.

While 41% of CS professionals report acting as the primary voice of the customer to product and leadership, nearly 16% say their organization has no formal VoC initiative at all.

In sales-first environments, voice-of-customer efforts often compete with pipeline urgency. Product teams may prioritize features that support new deals rather than long-term adoption improvements. Feedback loops can become reactive instead of systemic.

More importantly, VoC is often treated as input rather than constraint. Customer feedback may be heard, but it does not necessarily shape what is sold, how deals are structured, or which segments are targeted.

Over time, the absence of structured VoC investment limits an organization’s ability to align acquisition strategy with product-market reality.

In healthy systems, customer insight doesn’t compete with pipeline. It shapes pipeline by tightening ICP definition, informing pricing and packaging, and influencing which deals are celebrated internally.

Cultural shifts follow economic cycles

The 2025 shift toward sales-first cultures does not exist in a vacuum. Historically, economic slowdowns have prompted organizations to re-center on acquisition. When growth slows and capital tightens, leadership teams gravitate toward immediate revenue levers.

However, these shifts are rarely permanent. Culture responds to outcomes.

If acquisition intensity outpaces retention capacity for too long, churn rises and net revenue retention declines. When those signals appear, organizations recalibrate.

As we move through 2026, many leadership teams will likely begin evaluating the consequences of 2025’s strategic emphasis.

Did sales-first acceleration strengthen sustainable growth? Did expansion ownership clarify accountability or create ambiguity? Did customer-first principles erode, or integrate more deeply into commercial strategy?

These questions will shape the next phase of cultural alignment.

What high-performing organizations are doing differently

The strongest organizations are not choosing between sales-first and customer-first models. They’re integrating them deliberately.

In these environments:

- Revenue metrics are shared across functions, ensuring alignment between acquisition and retention.

- Incentives are structured to reflect long-term customer health, not just initial bookings.

- Adoption frameworks are formalized, making value delivery measurable and scalable.

- Enablement investment matches revenue accountability, equipping CS teams to fulfill commercial expectations.

- Customer success leadership maintains proximity to executive decision-making, reinforcing strategic influence.

In short, culture is designed rather than reactive.

A quick diagnostic for leadership teams

Many organizations don’t realize which culture they operate in until pressure exposes it.

For leaders trying to understand their own cultural balance, a few simple questions can reveal a great deal:

- What gets celebrated more loudly: the largest new logo or the largest multi-year expansion?

- Which metric opens executive meetings: new ARR, GRR/NRR, or customer outcome metrics?

- When budgets tighten, which teams are frozen first?

- Who has the authority to walk away from a misaligned deal?

The real question isn't “Are we sales-first or customer-first?” It’s whether the current mix of incentives, investments, and leadership attention creates the kind of growth the organization wants three years from now.

From acceleration to alignment in 2026

If 2025 was defined by urgency and revenue pressure, 2026 may be characterized by evaluation and alignment. Organizations that leaned heavily into sales-first thinking will assess retention stability.

Customer-first companies will evaluate whether their long-term strategies translate into measurable growth. Hybrid models will refine integration between acquisition and expansion teams.

The cultural pendulum rarely rests at extremes. It adjusts based on performance data. Customer success sits at the center of that adjustment.

The bottom line

Customer success is maturing. Revenue accountability is rising. Cultural emphasis is shifting.

Sales-first organizations are increasing. Customer-first cultures have declined. But the future does not belong exclusively to either model.

The organizations that thrive in 2026 will recognize that acquisition and retention aren’t competing priorities. They are components of a single growth system.

When culture aligns with both, growth becomes durable. When it does not, friction becomes expensive.

The next chapter of customer success will be defined not by which culture dominates, but by how well the two are integrated.

Help shape the next cultural benchmark

The State of Customer Success 2025 revealed a decisive shift toward sales-first cultures.

But what does that shift definitively look like in 2026? Has the pendulum continued to swing? Have customer-first organizations regained ground? Has expansion ownership strengthened alignment between sales and CS? Are budgets reinforcing post-sale infrastructure, or tightening further?

We’re currently gathering insights for the sixth edition of the State of Customer Success Report.

If you’re leading, building, or scaling customer success in 2026, your perspective will help define how the industry understands customer-first and sales-first culture in the year ahead.

Contribute to the 2026 survey and help shape the benchmark.

Become a CSC Insider

Thank you for subscribing

Get exclusive insights, frameworks, and strategies from customer success leaders driving real business impact.

An email has been successfully sent to confirm your subscription.

Follow us on LinkedIn

Follow us on LinkedIn